Understanding Bond Duration Introduction When stepping into the fixed-income market,...

Read More

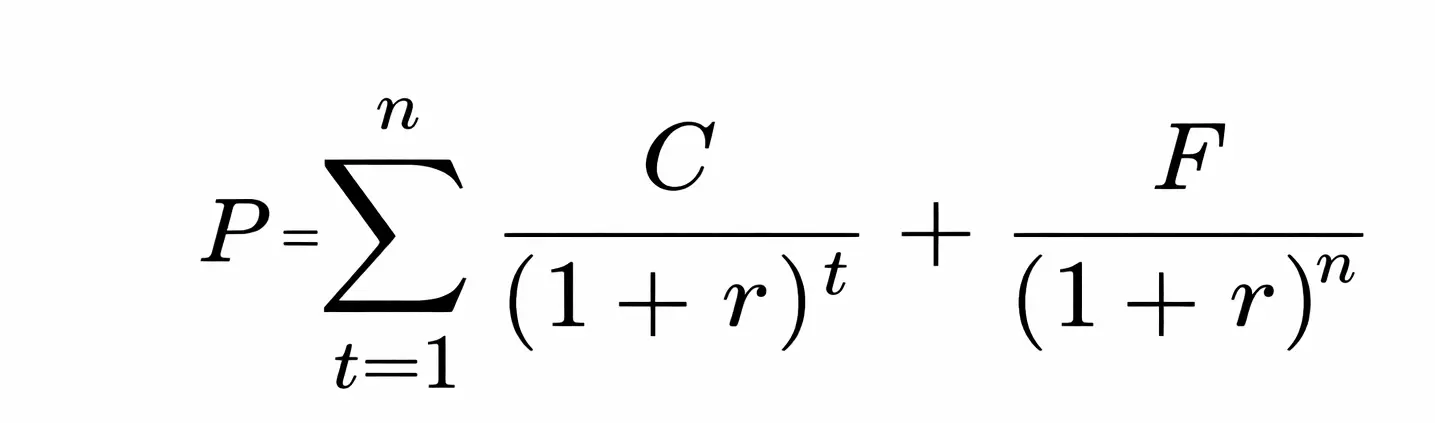

To calculate the price of a standard coupon-paying bond, analysts use the following formula:

Where:

- P = Current price of the bond.

- C = Periodic coupon payment (Coupon Rate × Face Value).

- r = Required rate of return or market yield (discount rate).

- t = The specific time period.

- n = Number of periods until maturity.

- F = Face value (Par value) of the bond.

This formula combines an annuity (the coupons) with a single future sum (the face value). By calculating each component, you can determine if a fixed income security is priced fairly relative to its risk.

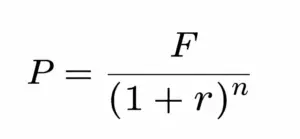

Because there are no intermediate cash flows, zero-coupon bonds are highly sensitive to changes in the bond yield vs interest rates environment. They are often used by institutional investors for long-term liability matching.

Bond Valuation Methods and Formulas

Bond Valuation Methods Mastering Bond Valuation Methods and Formulas: A...

Read More

The Inverse Relationship Between Bond Prices and Yields

The Inverse Relationship Between Bond Prices and Yields Table of...

Read More

Current Yield vs Yield to Maturity

Understanding Current Yield vs. Yield to Maturity Understanding Current Yield...

Read More

Bond Yield Vs Interest Rates

Bond Yield Vs Interest Rates Understanding the Relationship Between Bond...

Read More

Bond Yield to Maturity (YTM)

Bond Yield to Maturity (YTM) Understanding Bond Yield to Maturity...

Read More

Calculating Bond Price And Yield

Calculating Bond Price And Yield Understanding Bond Valuation: A Comprehensive...

Read More

Bond Pricing Fundamentals

Bond Pricing Fundamentals A Guide for Investors Table of Contents...

Read More

Short-Term, Intermediate, and Long-Term Bonds

Bond Maturities Short-Term, Intermediate, and Long-Term Bonds Table of Contents...

Read More

Investment Grade vs Non-Investment Grade Bonds

Investment Grade vs Non-Investment Grade Bonds A Guide for UAE...

Read More

Bonds: Face Value, Par Value & Coupon Rate

Bonds: Face Value, Par Value & Coupon Rate When venturing...

Read More

Bond Issuers Government vs Corporate Bonds

Bond Issuers Government vs Corporate Bonds What UAE Investors Need...

Read More

What is a Bond and How Does It Work?

What is a Bond and How Does It Work? A...

Read More

Understanding Bond Fundamentals: A Guide for Smart Investing

Understanding Bond Fundamentals: A Guide for Smart Investing In the...

Read More