Options Exercise & Assignment Table of Contents Introduction What Does...

Read More

American vs European Options

American vs European Options Table of Contents Introduction What Is...

Read More

Options Expiration Dates

Options Expiration Dates Table of Contents Introduction What Is an...

Read More

Options Strike Price

Options Strike Price Table of Contents Introduction What Is a...

Read More

Intrinsic Value and Time Value

Intrinsic Value and Time Value Introduction When you buy or...

Read More

In-the-Money, At-the-Money, Out-of-the-Money Options

In-the-Money, At-the-Money, Out-of-the-Money Options Introduction If you have started exploring...

Read More

Put Options Explained

Put Options Explained Table of Contents Introduction What Is a...

Read More

Call Options Explained

Call Options Explained Table of Contents Introduction What Exactly Is...

Read More

Options Fundamentals

Options Fundamentals Table of Contents Introduction What Is an Option...

Read More

Deferred Coupon Bonds

Perpetual Bonds Table of Contents Introduction What Are Deferred Coupon...

Read More

Perpetual Bonds

Perpetual Bonds Table of Contents Introduction What Are Perpetual Bonds?...

Read More

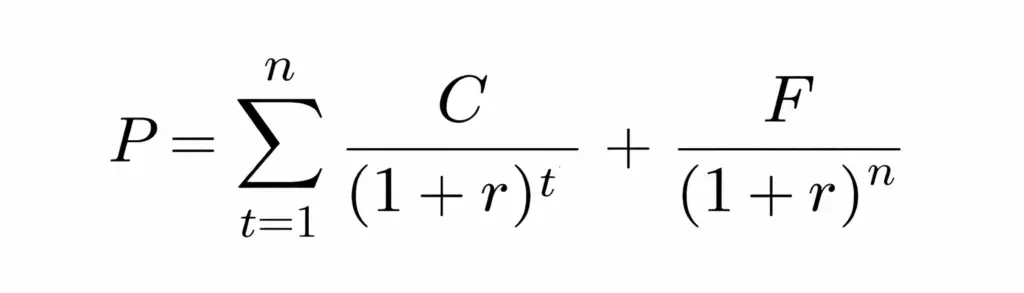

Inflation-Linked Bonds

Inflation-Linked Bonds Introduction Inflation is the silent tax that erodes...

Read More

Convertible Bonds Basics

Convertible Bonds Explained: Structure, Benefits, and Risks for Investors Table...

Read More

Callable and Putable Bonds

Callable and Putable Bonds Table of Contents Introduction What Is...

Read More

Floating Rate Bonds

Floating Rate Bonds Introduction Interest rates move. That is one...

Read More

Zero-Coupon Bonds

Zero-Coupon Bonds Introduction Most bonds pay you regular interest —...

Read More

Municipal Bonds and Tax Implications

Municipal Bonds & Tax Implications Introduction When investors look for...

Read More

Corporate Bonds and Corporate Credit

Government Bonds & Treasury Securities Guide Table of Contents Introduction...

Read More

Government Bonds & Treasury Securities

Government Bonds & Treasury Securities Guide Introduction When markets get...

Read More

Bollinger Bands Strategy

Bollinger Bands Strategy Introduction Every trader, at some point, asks...

Read More

Moving Average Crossover

Moving Average Crossover Introduction Every trader, whether new or experienced,...

Read More

Support-Resistance Bounce

Support/Resistance Bounce Table of Contents Introduction What Is Support and...

Read More

Breakout Trading

Breakout Trading Introduction Every experienced trader knows that markets don’t...

Read More

Mean Reversion

Mean Reversion Table of Contents Introduction What Is Mean Reversion...

Read More

Momentum Trading

Momentum Trading Table of Contents What Is Momentum Trading? How...

Read More

Trend Following Strategy

Trend Following Strategy Introduction Most traders spend years trying to...

Read More

Contingent Conversion Features

Contingent Conversion Features Introduction Structured products have evolved considerably over...

Read More

Early Redemption Features

Early Redemption Features Table of Contents Introduction What Is an...

Read More

Coupon Payments in Autocalls

Coupon Payments in Autocalls Table of Contents Introduction What Is...

Read More

Observation Dates

Observation Dates Introduction If you have ever explored structured products...

Read More