Perpetual Bonds Table of Contents Introduction What Are Deferred Coupon...

Read MoreGovernment Bonds & Treasury Securities Guide

Introduction

When markets get choppy, investors instinctively look for safer ground. Government bonds and treasury securities have long served as that ground — steady, backed by sovereign governments, and offering predictable returns. Whether you are building a balanced portfolio, managing risk, or simply looking to diversify beyond equities, understanding how these instruments work is essential.

This guide breaks down everything you need to know — from the basics of what a government bond actually is, to the different types available, how they’re priced, and what risks you should be aware of before investing.

Table of Contents

- What Is a Government Bond?

- What Are Treasury Securities?

- What Are the Main Types of Treasury Securities?

- How Do Government Bonds Generate Returns?

- What Is the Relationship Between Bond Prices and Interest Rates?

- Are Government Bonds Risk-Free?

- How Do Government Bonds Fit Into a Portfolio?

- Can Investors Outside the US Access These Securities?

- Conclusion & Key Takeaways

What Is a Government Bond?

A government bond is a debt instrument issued by a national government to raise money from investors. When you buy a government bond, you are effectively lending money to the government. In return, the government promises to pay you regular interest (called the coupon) over the life of the bond and return your original investment (the principal) when the bond matures.

Governments issue bonds to fund public spending — infrastructure projects, healthcare, education, or to cover budget deficits. Because these bonds are backed by the full faith and credit of a sovereign government, they are widely regarded as among the safest investments available in global capital markets.

The key features of a government bond include:

- Face Value (Par Value): The amount the government will repay at maturity — typically USD 1,000 or equivalent.

- Coupon Rate: The annual interest rate paid on the face value.

- Maturity Date: The date when the principal is repaid and the bond expires.

- Yield: The actual return an investor earns based on the bond’s current market price.

If you’re still building your understanding of bond terminology, the bond basics on our blog pages is a solid starting point before diving deeper into specific bond types.

What Are Treasury Securities?

Treasury securities are government bonds specifically issued by the United States Department of the Treasury. They are the most widely traded sovereign debt instruments in the world and serve as a global benchmark for risk-free returns.

Because the US government has never defaulted on its debt obligations, treasury securities are used by institutional investors, central banks, pension funds, and individual investors worldwide as a safe store of value and a benchmark against which other investments are measured.

The yield on US Treasury securities — particularly the 10-year note — is one of the most closely watched indicators in global finance, influencing everything from mortgage rates to corporate bond pricing to equity valuations.

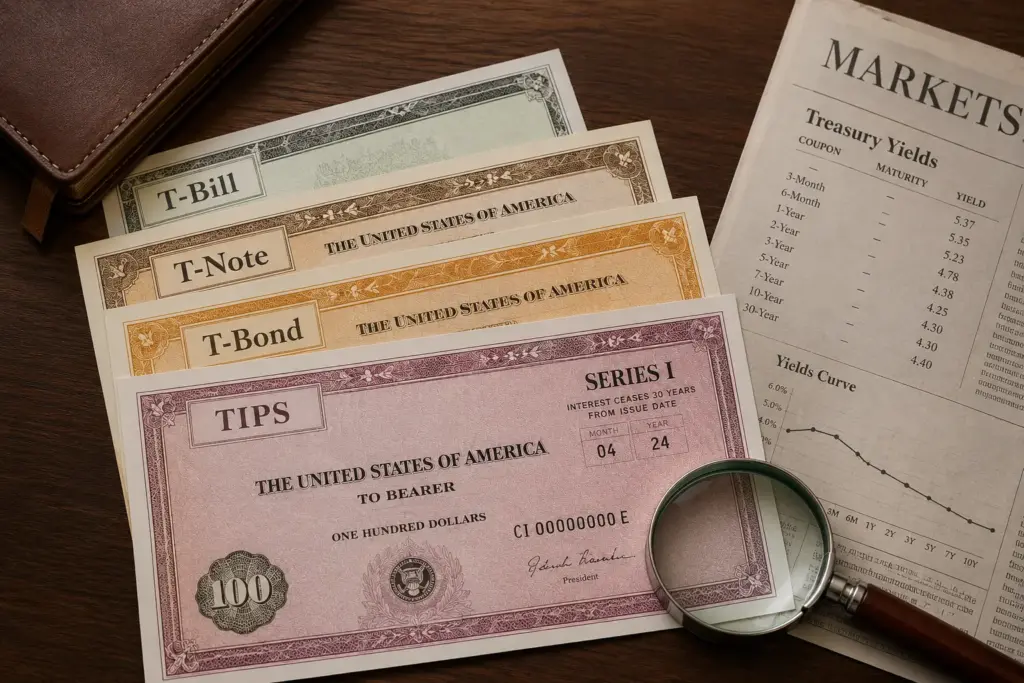

What Are the Main Types of Treasury Securities?

Not all government bonds are alike. They differ primarily by their maturity period, which affects how much interest they pay and how sensitive they are to market conditions.

Treasury Bills (T-Bills)

T-Bills are short-term securities that mature in 4, 8, 13, 26, or 52 weeks. They don’t pay a regular coupon. Instead, they are sold at a discount to their face value, and the investor receives the full face value at maturity. The difference between what you paid and what you receive is your return.

Example: You purchase a T-Bill for USD 970. At maturity, you receive USD 1,000. Your gain of USD 30 is your effective interest.

Treasury Notes (T-Notes)

T-Notes are medium-term instruments with maturities of 2, 3, 5, 7, or 10 years. Unlike T-Bills, they pay a fixed coupon every six months, making them popular with investors seeking regular income. The 10-year Treasury Note is the most referenced bond globally.

Treasury Bonds (T-Bonds)

T-Bonds are long-term instruments with maturities of 20 or 30 years. They pay semi-annual coupons and are preferred by long-horizon investors such as pension funds and insurance companies that need to match long-term liabilities with long-term income.

Treasury Inflation-Protected Securities (TIPS)

TIPS are designed to protect investors against inflation. The principal value of a TIPS adjusts with changes in the Consumer Price Index (CPI). As inflation rises, so does the face value of the bond — and thus the interest payment, which is calculated on the adjusted principal. This makes TIPS especially relevant in high-inflation environments.

Sovereign Bonds From Other Governments

Beyond US Treasuries, sovereign bonds are issued by governments worldwide — UK Gilts, German Bunds, Japanese Government Bonds (JGBs), and bonds from GCC nations including Saudi Arabia and the UAE. These bonds operate on the same fundamental principles but carry different risk profiles depending on each country’s credit rating, economic stability, and currency.

Diversify your portfolio with sovereign and corporate bonds.

PhillipCapital DIFC gives you access to a wide range of fixed income instruments across global markets.

How Do Government Bonds Generate Returns?

Government bonds generate returns through two primary channels:

- Coupon Income If the bond pays a coupon (as T-Notes and T-Bonds do), you receive fixed interest payments at regular intervals — typically every six months. This makes government bonds attractive for income-focused investors who want predictable cash flows regardless of market conditions.

- Capital Appreciation (or Depreciation) Bond prices move in the secondary market. If you purchase a bond and interest rates in the economy fall after your purchase, your bond (which pays a higher fixed coupon) becomes more valuable — and you can sell it at a price above what you paid. Conversely, if rates rise, the price of your existing bond falls.

- Discount-to-Face Value (for T-Bills) As explained earlier, T-Bills are issued at a discount. The return is built into the difference between purchase price and face value at maturity.

Understanding how these returns are calculated is closely tied to bond pricing and valuation concepts. The bond pricing and valuation section walks through yield calculations in practical detail.

What Is the Relationship Between Bond Prices and Interest Rates?

This is one of the most important concepts in fixed income investing, and it’s surprisingly straightforward once you see it clearly.

Bond prices and interest rates move in opposite directions. This is an inverse relationship.

Here’s why: Suppose you hold a bond paying a 4% annual coupon. Now suppose market interest rates rise to 6%. New bonds being issued will offer 6%, making your 4% bond less attractive. To sell your bond, you’d need to lower its price so the buyer effectively earns a competitive return.

The reverse is also true. If interest rates fall to 2%, your 4% bond looks very attractive — investors will pay a premium above face value to own it.

This relationship has critical implications for portfolio management, particularly for long-duration bonds. A bond with a 30-year maturity is far more sensitive to interest rate changes than a 2-year note. This sensitivity is measured by a concept called duration, which you can explore further in the bond duration and risk section.

Are Government Bonds Risk-Free?

Government bonds — particularly US Treasuries — are often called “risk-free.” But that’s not entirely accurate. While the risk of outright default is extremely low for stable sovereign governments, other risks do exist:

Interest Rate Risk: As discussed, rising rates reduce the market value of existing bonds. This matters if you plan to sell before maturity.

Inflation Risk: If inflation outpaces your bond’s coupon rate, the real purchasing power of your returns erodes. TIPS are specifically designed to address this.

Currency Risk: If you invest in a foreign government bond (say, Japanese JGBs in yen) and your home currency strengthens, your returns in your local currency could be diminished.

Reinvestment Risk: When coupon payments are received, they may need to be reinvested at lower rates if market yields have declined.

Liquidity Risk: While US Treasuries are highly liquid, bonds from smaller sovereign issuers can be harder to sell quickly at fair prices.

Understanding these risks is essential before building any fixed income allocation. The bond types and structures section provides additional context on how different bond structures carry different risk profiles.

How Do Government Bonds Fit Into a Portfolio?

Government bonds serve several strategic purposes in a well-constructed investment portfolio:

Capital Preservation: For conservative investors or those nearing retirement, government bonds help preserve capital while generating modest income.

Diversification: Bonds typically have low or negative correlation with equities. When stock markets fall, investors often flock to government bonds (the “flight to safety”), which can push bond prices up and cushion overall portfolio losses.

Income Generation: Regular coupon payments provide predictable cash flow — valuable for retirees, institutions, or anyone relying on their investments for living expenses.

Benchmark Anchoring: Portfolio managers often use treasury yields as a baseline when evaluating the risk-return of other assets. If a riskier investment doesn’t offer a meaningful return above the treasury yield, it may not be worth the added risk.

For investors already active in equities or derivatives, adding fixed income instruments like government bonds through a trusted broker can meaningfully reduce overall portfolio volatility. If you’re curious about combining these with structured products, the wealth management and structured notes page outlines how tailored strategies are built around your goals.

Explore Institutional-Grade Investment Solutions

For sophisticated investors seeking tailored fixed income strategies. Our institutional services team works with funds and family offices across the MENA region.

Can Investors Outside the US Access These Securities?

Absolutely. US Treasury securities are among the most accessible investment instruments in the world. International investors — including those based in the UAE and broader Middle East — can access them through licensed brokers, international custodians, and global fixed income platforms.

For UAE-based investors specifically, government bond investing is well within reach through platforms like PhillipCapital DIFC, which provides regulated access to global fixed income markets from within the Dubai International Financial Centre.

It’s worth noting that many Gulf sovereign bonds — including those issued by UAE and Saudi government entities — are also actively traded internationally and carry investment-grade ratings from global agencies, making them compelling options for regional investors seeking local market exposure with fixed income characteristics.

Conclusion & Key Takeaways

Government bonds and treasury securities form the bedrock of the global fixed income universe. They are instruments of stability, income, and strategic diversification — used by everyone from individual savers to the world’s largest sovereign wealth funds.

Here’s what to remember:

- Government bonds are loans to sovereign governments, repaid with interest over a defined term.

- US Treasury securities (T-Bills, T-Notes, T-Bonds, TIPS) are the global benchmark for sovereign debt.

- Bond prices move inversely to interest rates — a fundamental rule every investor must understand.

- While considered low-risk, government bonds still carry interest rate, inflation, and currency risks.

- They play a vital role in portfolio diversification, capital preservation, and income generation.

- International investors, including those in the UAE, have full access to global government bond markets through regulated brokers.

Whether you are exploring fixed income for the first time or looking to refine an existing strategy, government bonds deserve a clear, informed place in your investment thinking.

Start Investing in Global Fixed Income

Open a trading account with PhillipCapital DIFC and access sovereign bonds across global markets.

Frequently Asked Questions (FAQs)

Is it possible to lose money on government bonds?

Yes — but only if you sell before maturity. If you hold a government bond to its maturity date, you receive your full principal back as promised. The risk kicks in when you sell in the secondary market. If interest rates have risen since you bought the bond, its market price will be lower, and selling at that point means a loss. For buy-and-hold investors, this risk is largely irrelevant.

What is the difference between a T-Bill and a T-Bond?

The main difference is time. A T-Bill matures in under a year and pays no regular interest — you simply buy it at a discount and collect the face value at maturity. A T-Bond has a 20 or 30-year term and pays fixed interest every six months. T-Bills suit short-term cash management; T-Bonds suit long-term income planning.

Are government bond returns taxed?

It depends on the country. US Treasury interest is exempt from state and local taxes but is taxable at the federal level. For UAE-based investors, there is no personal income tax, which means coupon income from foreign government bonds is generally not taxed locally. Always verify the tax treatment in your jurisdiction before investing.

Why do investors buy government bonds when the returns are low compared to stocks?

Because returns are only part of the equation. Government bonds offer capital preservation, predictable income, and lower volatility — things stocks cannot guarantee. During market downturns, investors typically shift money into government bonds as a safe haven, which can actually push bond prices up. In a balanced portfolio, bonds act as a buffer against equity losses, not a replacement for growth.

Disclaimer:

Trading foreign exchange and/or contracts for difference on margin carries a high level of risk, and may not be suitable for all investors as you could sustain losses in excess of deposits. The products are intended for retail, professional and eligible counterparty clients. Before deciding to trade any products offered by PhillipCapital (DIFC) Private Limited you should carefully consider your objectives, financial situation, needs and level of experience. You should be aware of all the risks associated with trading on margin. The content of the Website must not be construed as personal advice. For retail, professional and eligible counterparty clients. Before deciding to trade any products offered by PhillipCapital (DIFC) Private Limited you should carefully consider your objectives, financial situation, needs and level of experience. You should be aware of all the risks associated with trading on margin.

Rolling Spot Contracts and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 78% of our retail client accounts lose money while trading with us. You should consider whether you understand how Rolling Spot Contracts and CFDs work, and whether you can afford to take the high risk of losing your money.

Inflation-Linked Bonds

Inflation-Linked Bonds Introduction Inflation is the silent tax that erodes...

Read More

Convertible Bonds Basics

Convertible Bonds Explained: Structure, Benefits, and Risks for Investors Table...

Read More

Callable and Putable Bonds

Callable and Putable Bonds Table of Contents Introduction What Is...

Read More

Municipal Bonds and Tax Implications

Municipal Bonds & Tax Implications Introduction When investors look for...

Read More

Corporate Bonds and Corporate Credit

Government Bonds & Treasury Securities Guide Table of Contents Introduction...

Read More

Government Bonds & Treasury Securities

Government Bonds & Treasury Securities Guide Introduction When markets get...

Read More