Contingent Conversion Features Introduction Structured products have evolved considerably over...

Read MoreCoupon Payments in Autocalls

Table of Contents

- Introduction

- What Is an Autocall and Why Do Coupon Payments Matter?

- How Are Coupon Payments Structured in an Autocall?

- What Is a Conditional Coupon — And When Is It Paid?

- What Is a Memory Coupon Feature and How Does It Work?

- How Does the Autocall Trigger Affect Coupon Income?

- What Happens to Coupons If the Product Is Not Called?

- Are Coupon Payments in Autocalls Guaranteed?

- How Do Autocall Coupons Compare to Traditional Bond Income?

- Key Takeaways & Conclusion

Introduction

When investors explore structured products, one of the most commonly asked questions is: how do I actually earn income from these instruments? For autocallable products — commonly known as autocalls — the answer lies in understanding how coupon payments are designed, when they are triggered, and what conditions must be met for them to be paid out.

Autocalls have grown significantly in popularity among yield-seeking investors globally, particularly in wealth management circles across the UAE and the broader Middle East. They offer the potential for above-market income, but that income comes with specific rules. Before exploring the coupon mechanics in detail, it helps to have a solid foundation in how structured products work so you can place autocall coupons within the broader context of structured investment design.

What Is an Autocall and Why Do Coupon Payments Matter?

An autocall (short for “automatically callable”) is a type of structured product that can be redeemed before its scheduled maturity date — automatically — if certain market conditions are met on predefined observation dates. These conditions typically revolve around the performance of an underlying asset, such as an equity index, a basket of stocks, or a single stock.

The coupon is the income component of the autocall. Unlike a standard dividend or bond interest, the coupon in an autocall is not simply handed to the investor on a fixed calendar date regardless of market conditions. Instead, it is linked — directly or indirectly — to how the underlying asset performs. This is what makes autocalls both attractive and more nuanced than traditional income instruments.

For investors who want to move beyond simple fixed income and explore yield-enhancement strategies, understanding the coupon structure of an autocall is the essential starting point. If you are new to this space, our introduction to structured products basics provides valuable context on how these instruments fit into a modern investment portfolio.

How Are Coupon Payments Structured in an Autocall?

Autocall coupons are defined at the point of issuance and expressed as an annualised rate — for example, 10% per annum — but the actual payment schedule depends on the product’s structure.

At the most basic level, the issuer sets:

- The coupon rate — the annual income percentage applied to the notional investment amount.

- Observation dates — specific dates (monthly, quarterly, semi-annually) when the underlying asset’s level is measured.

- The coupon barrier — a price threshold the underlying must be at or above for the coupon to be paid on that observation date.

For example, if the coupon barrier is set at 70% of the initial asset level, the investor receives a coupon payment on every observation date where the underlying is trading at or above that 70% threshold. If it falls below, no coupon is paid for that period — though certain structures allow missed coupons to be recovered later, which we cover in the memory coupon section below.

This conditional structure is what makes autocall coupons genuinely different from bond coupons. They offer higher income potential precisely because the investor accepts the risk of not receiving income during periods of poor market performance. Understanding this trade-off is central to understanding the risk and return profile of any autocallable product.

What Is a Conditional Coupon — And When Is It Paid?

A conditional coupon is one that is only paid if the underlying asset meets a specified condition on the observation date. This is the most common coupon type found in autocall structures.

The condition is almost always expressed as a level relative to the asset’s starting price — known as the “initial fixing level.” Typical coupon barriers range from 50% to 80% of this starting level, meaning the product offers a significant buffer before income is interrupted.

Here is a practical illustration: Suppose you invest in an autocall linked to a major equity index, with a 12% annual coupon and a coupon barrier at 70% of the initial level. If the index is observed quarterly:

- On each quarterly observation date, if the index is at or above 70% of its starting level, you receive 3% (a quarter of the 12% annual rate).

- If the index is below that 70% level on any observation date, no coupon is paid for that quarter.

This design is particularly appealing in sideways or mildly bearish markets, where traditional equities might disappoint but the underlying can still remain above the coupon barrier, keeping income flowing. It is also why autocalls are frequently categorised under yield-enhancement structured products, a category you can explore further in the types of structured products section.

Explore Structured Investment Solutions

Discover tailored structured notes designed to match your income goals and risk appetite

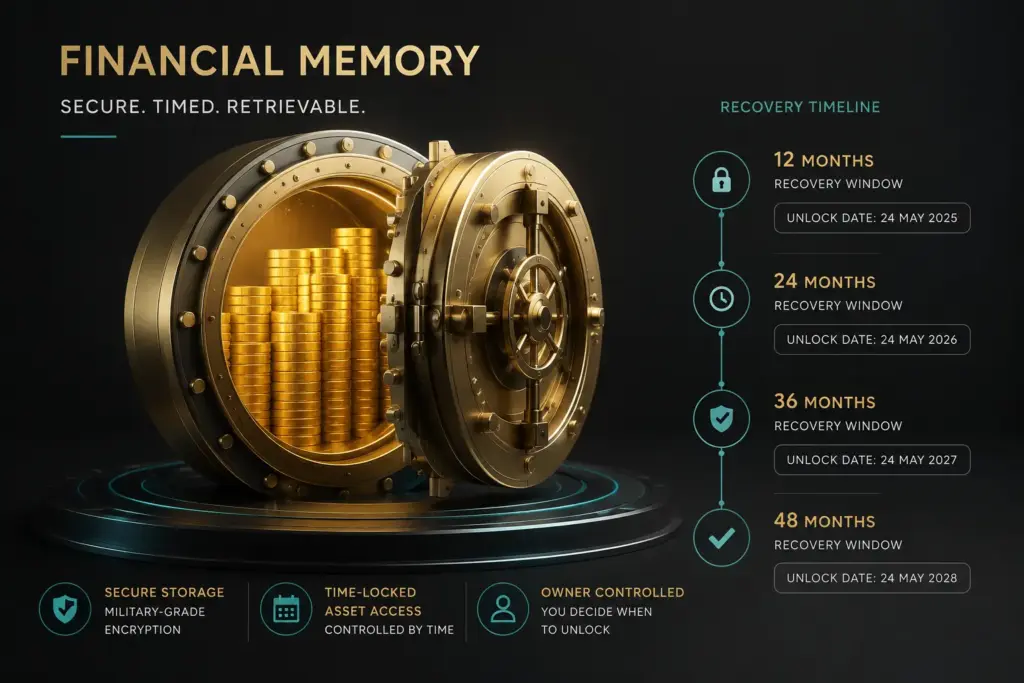

What Is a Memory Coupon Feature and How Does It Work?

The memory coupon (also called a “coupon memory” or “accumulation feature”) is a mechanism that allows previously missed coupon payments to be recovered and paid out when the underlying asset eventually returns to or above the coupon barrier.

This feature significantly changes the risk profile of the product for income-oriented investors. Without memory, a missed coupon is simply lost — gone forever. With memory, the product “remembers” every unpaid coupon and accumulates them. When conditions are next met — either at a future observation date or at the autocall trigger — all accumulated unpaid coupons are released at once.

To illustrate: suppose an autocall pays quarterly and the underlying drops below the barrier for two consecutive quarters, resulting in two missed coupons of 3% each. On the third quarter, the underlying recovers and closes above the barrier. With a memory coupon feature, the investor receives not just the current quarter’s 3%, but also the two previously missed coupons — a total payment of 9% in that single period.

This is one of the most investor-friendly design features available in modern autocall structures. It makes the product particularly appealing to investors who are willing to weather a short period of market weakness in exchange for the potential to receive a larger lump-sum coupon payment when markets recover. Memory coupons are more commonly found in products designed for professional investors or within discretionary wealth management mandates, such as those offered through institutional services.

How Does the Autocall Trigger Affect Coupon Income?

The autocall trigger — the level at which the product is automatically redeemed early — is directly connected to the coupon story because once the product is called, no further coupons are paid.

The autocall trigger is typically set at or above the initial asset level (for example, 100% of the starting price). On each observation date, if the underlying is at or above this trigger level, the product terminates early, returning the investor’s capital plus the coupon due for that period and, in some structures, any accumulated memory coupons.

This creates an important consideration: early redemption is generally a positive event for the investor — capital is returned with income intact — but it also means the investment stops generating future coupons. In a rising market, this could mean the product ends after just one or two quarters, leaving the investor to reinvest at potentially different terms.

Conversely, if markets remain range-bound or slightly below the autocall trigger but above the coupon barrier, the investor continues to collect coupons for longer without early redemption. Some investors actually prefer this scenario for its income-generating potential over a longer period. The interplay between the autocall trigger and coupon collection is one of the more nuanced aspects of structured product design, and understanding it requires a clear view of how knock-in and knock-out features interact within the same product.

What Happens to Coupons If the Product Is Not Called?

If the autocall trigger is never met throughout the life of the product and it runs to its scheduled maturity date, the coupon structure follows its originally defined terms — though the outcome depends on the product’s final performance.

In most standard autocall structures, the following applies at maturity:

- If the underlying is at or above the capital protection barrier (often 60%–70% of the initial level), the investor receives their full capital back, plus any final coupon due.

- If the underlying has fallen below the capital protection barrier — often called the “knock-in” level — the investor may receive back less than their original investment, with the loss reflecting the degree of the asset’s decline.

On the coupon side at maturity, whether final coupon is paid typically depends on where the underlying closes relative to the coupon barrier. Some products also include a “final coupon regardless” clause if the capital is returned in full, though this varies by issuer and structure.

For investors who want to understand the full spectrum of capital risk in these scenarios, our guides on full capital protection, partial capital protection, and zero capital protection outline how capital outcomes differ across different autocall designs.

Speak With Our Structured Products Team

Our specialists can walk you through autocall coupon structures that fit your investment objectives.

Are Coupon Payments in Autocalls Guaranteed?

No — coupon payments in autocalls are not guaranteed. This is one of the most important points any investor must understand before committing capital to an autocallable product.

The conditional nature of coupon payments is precisely why these products can offer higher income than traditional fixed deposits or government bonds. The investor is accepting the risk that coupons may not be paid in periods of poor market performance. However, “not guaranteed” does not mean “likely to be lost.” The product’s structure — particularly the level of the coupon barrier — is designed to provide a meaningful buffer.

For example, a coupon barrier set at 60% of the initial asset level means the underlying would need to lose 40% of its value before coupons begin to be missed. Historically, such declines are possible but not the norm across short to medium-term time horizons for major indices.

The key factors that affect coupon payment probability are: the depth of the coupon barrier, the volatility of the underlying asset, the observation frequency, and the presence or absence of a memory feature. Products linked to highly volatile underlyings will, by design, carry more coupon uncertainty — and typically offer higher stated coupon rates to compensate for this. Understanding the components of a structured product in detail is essential here, and our piece on components of structured products breaks down each element clearly.

How Do Autocall Coupons Compare to Traditional Bond Income?

Autocall coupons and bond coupons serve similar purposes — providing periodic income to investors — but they differ meaningfully in their certainty, their size, and the conditions under which they are paid.

Traditional bonds pay a fixed interest rate (the coupon) on a predetermined schedule regardless of market conditions, provided the issuer does not default. This makes bond income predictable and dependable. However, in a low-to-moderate yield environment, investment-grade bond coupons can be modest, especially after adjusting for inflation.

Autocall coupons, by contrast, are conditional but typically offer substantially higher stated rates — often two to five times the prevailing bond yield for equivalent maturities — in exchange for accepting the conditional payment risk and the possibility of loss at maturity if markets fall sharply.

The comparison can be summarised as: bonds give you certainty at a lower income rate; autocalls give you higher potential income at the cost of conditionality. For investors who hold a core bond portfolio and want to add a layer of enhanced yield exposure, autocalls serve as a complementary rather than replacement tool. If you are building a diversified income strategy, it is worth understanding how bonds and debentures can sit alongside structured notes for a balanced approach to income generation.

Access Global Investment Solutions

Open an account with PhillipCapital DIFC to access structured notes and income products.

Key Takeaways & Conclusion

Coupon payments are at the heart of what makes autocallable structured products an attractive income solution — but they come with an important layer of conditionality that investors must fully understand.

Here are the essential points to carry forward:

- Autocall coupons are conditional, not guaranteed. They are paid only when the underlying asset is at or above the coupon barrier on observation dates.

- The coupon barrier provides a buffer — typically set well below the starting asset level — meaning coupons can continue to be paid even in moderately declining markets.

- Memory coupon features allow previously missed coupons to accumulate and be paid in a lump sum when conditions recover, making these products more forgiving during short-term market weakness.

- The autocall trigger and coupon income are linked — early redemption is generally positive but ends future income; longer non-call periods allow income to build.

- Higher coupon rates reflect higher conditionality risk — products linked to more volatile underlyings or with more stringent coupon conditions tend to offer higher stated rates.

- Autocall coupons are not a substitute for bond income but can complement a fixed-income portfolio as a yield-enhancement strategy for investors with appropriate risk appetite.

For investors in the UAE and across the Middle East looking to explore autocallable products as part of a broader wealth strategy, working with an experienced and regulated brokerage partner is essential. PhillipCapital DIFC, regulated by the DFSA and part of a group with over 50 years of financial services experience, provides access to structured investment solutions designed for both retail and professional clients.

Whether you are new to structured products or looking to deepen your understanding of specific product mechanics, our full library of structured products learning resources is a strong next step.

Frequently Asked Questions (FAQs)

What happens to my coupon if the market drops below the barrier on an observation date?

You simply don’t receive a coupon for that period. The payment is skipped — not cancelled permanently in all cases. If your autocall has a memory coupon feature, those missed amounts accumulate and are paid out together the next time the underlying recovers above the barrier. Without a memory feature, the missed coupon is gone for good. This is one of the most misunderstood aspects of autocall income, so always confirm whether your product includes coupon memory before investing.

Can I lose money even if I received coupons during the product's life?

Yes, you can. Coupons and capital protection are two separate things in an autocall. Receiving regular coupon payments throughout the term does not protect your principal at maturity. If the underlying asset has fallen below the capital barrier (knock-in level) by maturity and the product was never called, you could receive back less than you invested — regardless of how much income you collected along the way. Always review the knock-in terms before committing.

Why do autocall coupons look so much higher than regular savings or bond rates?

Because the income is conditional, not guaranteed. Banks and issuers can offer higher rates precisely because the investor is accepting the risk that coupons may not be paid if markets fall. It’s a risk-return trade-off — not a free lunch. The higher the coupon rate offered, the greater the conditionality or the higher the volatility of the underlying asset linked to the product.

If the autocall is triggered early, do I get all my remaining coupons?

No. Once the autocall trigger is hit on an observation date, the product terminates. You receive your capital back plus the coupon due for that period (and any accumulated memory coupons, if applicable) — but no future coupons, since the product no longer exists. Early redemption is generally a positive outcome, but it does end your income stream sooner than expected.

Disclaimer:

Trading foreign exchange and/or contracts for difference on margin carries a high level of risk, and may not be suitable for all investors as you could sustain losses in excess of deposits. The products are intended for retail, professional and eligible counterparty clients. Before deciding to trade any products offered by PhillipCapital (DIFC) Private Limited you should carefully consider your objectives, financial situation, needs and level of experience. You should be aware of all the risks associated with trading on margin. The content of the Website must not be construed as personal advice. For retail, professional and eligible counterparty clients. Before deciding to trade any products offered by PhillipCapital (DIFC) Private Limited you should carefully consider your objectives, financial situation, needs and level of experience. You should be aware of all the risks associated with trading on margin.

Rolling Spot Contracts and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 78% of our retail client accounts lose money while trading with us. You should consider whether you understand how Rolling Spot Contracts and CFDs work, and whether you can afford to take the high risk of losing your money.

Early Redemption Features

Early Redemption Features Table of Contents Introduction What Is an...

Read More

Coupon Payments in Autocalls

Coupon Payments in Autocalls Table of Contents Introduction What Is...

Read More

Observation Dates

Observation Dates Introduction If you have ever explored structured products...

Read More

Autocall Mechanics

Autocall Mechanics Introduction If you’ve come across the term “autocallable...

Read More

Autocallable Structures

Autocallable Structure Table of Contents Introduction What Is an Autocallable...

Read More

Knock-In and Knock-Out Features

Knock-In and Knock-Out Features Table of Contents Introduction What Are...

Read More

Participation Structures in Structured Products

Participation Structures Maximizing Market Opportunities: A Guide to Participation Structures...

Read More

Zero Capital Protection

Zero Capital Protection Understanding Zero Capital Protection: Risks, Rewards, and...

Read More

Full Capital Protection

Full Capital Protection Understanding Full Capital Protection in Structured Products:...

Read More

Partial Capital Protection

Partial Capital Protection Partial Capital Protection: The Strategic Bridge Between...

Read More

Capital Protection Structures

Capital Protection Structures Strategic Wealth Preservation: A Comprehensive Guide to...

Read More

How Structured Products Work

How Structured Products Work A Complete Guide for Investors Table...

Read More

Components of Structured Products

Components of Structured Products A Detailed Guide for UAE Investors...

Read More

Introduction to Structured Products

Introduction to Structured Products In today’s dynamic financial landscape, traditional...

Read More