One-Touch and No-Touch Features Table of Contents Introduction What Are...

Read More

Barrier Levels and Payoff Impact

Barrier Levels and Payoff Impact Introduction Structured products often look...

Read More

Continuous vs Discrete Observation

Continuous vs Discrete Observation Table of Contents Introduction What Does...

Read More

Knock-Out Barriers

Knock-Out Barriers Table of Contents Introduction What Is a Knock-Out...

Read More

Knock-In Barriers

Knock-In Barriers Introduction If you have ever looked at a...

Read More

Barrier Levels and Types

Barrier Levels and Types Introduction Structured products are built around...

Read More

Contingent Conversion Features

Contingent Conversion Features Introduction Structured products have evolved considerably over...

Read More

Early Redemption Features

Early Redemption Features Table of Contents Introduction What Is an...

Read More

Coupon Payments in Autocalls

Coupon Payments in Autocalls Table of Contents Introduction What Is...

Read More

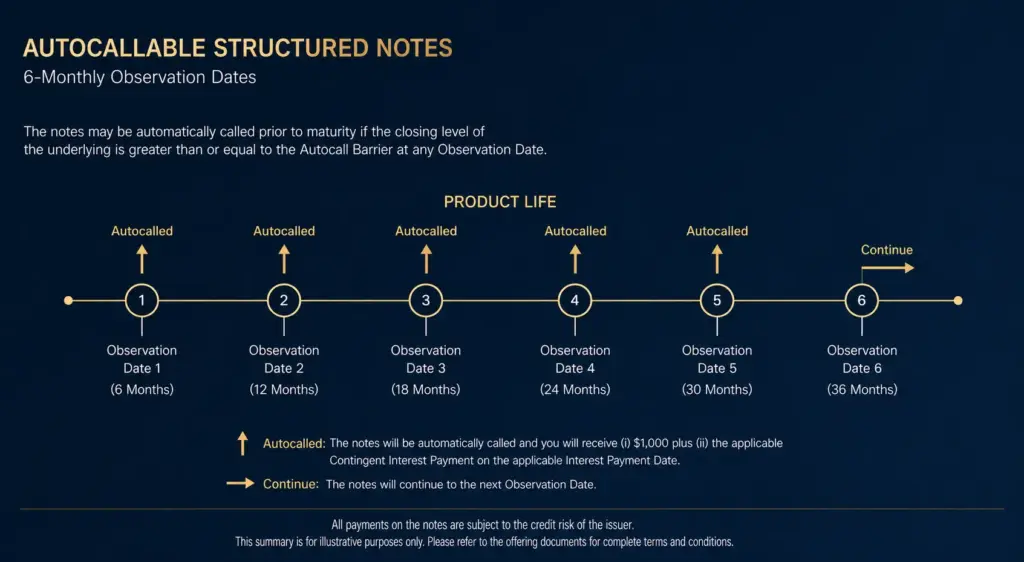

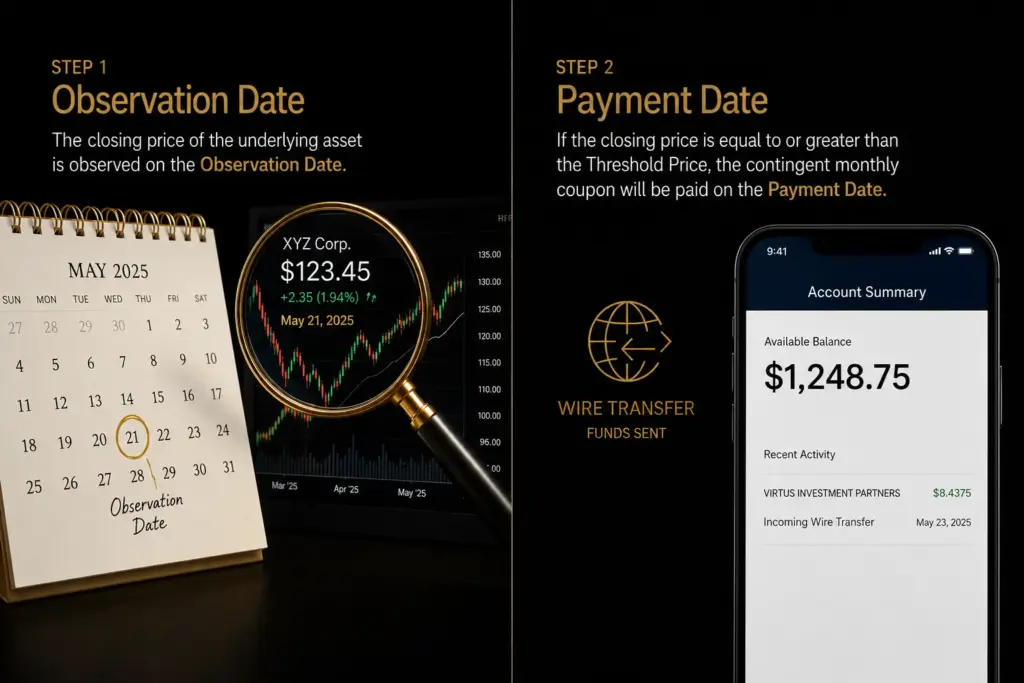

Observation Dates

Observation Dates Introduction If you have ever explored structured products...

Read More

Autocall Mechanics

Autocall Mechanics Introduction If you’ve come across the term “autocallable...

Read More

Autocallable Structures

Autocallable Structure Table of Contents Introduction What Is an Autocallable...

Read More

Knock-In and Knock-Out Features

Knock-In and Knock-Out Features Table of Contents Introduction What Are...

Read More

Turbo Structures

Turbo Structures Introduction In the dynamic world of global investing,...

Read More

Participation Structures in Structured Products

Participation Structures Maximizing Market Opportunities: A Guide to Participation Structures...

Read More

Zero Capital Protection

Zero Capital Protection Understanding Zero Capital Protection: Risks, Rewards, and...

Read More

Full Capital Protection

Full Capital Protection Understanding Full Capital Protection in Structured Products:...

Read More

Partial Capital Protection

Partial Capital Protection Partial Capital Protection: The Strategic Bridge Between...

Read More

Capital Protection Structures

Capital Protection Structures Strategic Wealth Preservation: A Comprehensive Guide to...

Read More

Risk and Return Profile

Understanding the Risk and Return Profile A Guide for Strategic...

Read More

How Structured Products Work

How Structured Products Work A Complete Guide for Investors Table...

Read More

Structured Notes

Structured Notes The Complete Guide to Tailored Wealth Management in...

Read More

Components of Structured Products

Components of Structured Products A Detailed Guide for UAE Investors...

Read More

Introduction to Structured Products

Introduction to Structured Products In today’s dynamic financial landscape, traditional...

Read More