One-Touch and No-Touch Features Table of Contents Introduction What Are...

Read MoreAutocall Mechanics

Introduction

If you’ve come across the term “autocallable product” and wondered what actually happens inside one — you’re not alone. These instruments sit at the heart of modern structured investing, offering a smart balance between yield potential and defined risk. But their inner workings — autocall triggers, observation dates, barrier levels — can seem like a maze without a proper guide.

This blog breaks down autocall mechanics in plain language, walking you through every key concept so you can evaluate these products with confidence. Whether you’re exploring structured notes for the first time or looking to deepen your existing understanding, this guide is built for you.

What Is an Autocallable Product?

What exactly is an autocallable structured product, and how does it differ from a regular bond or note?

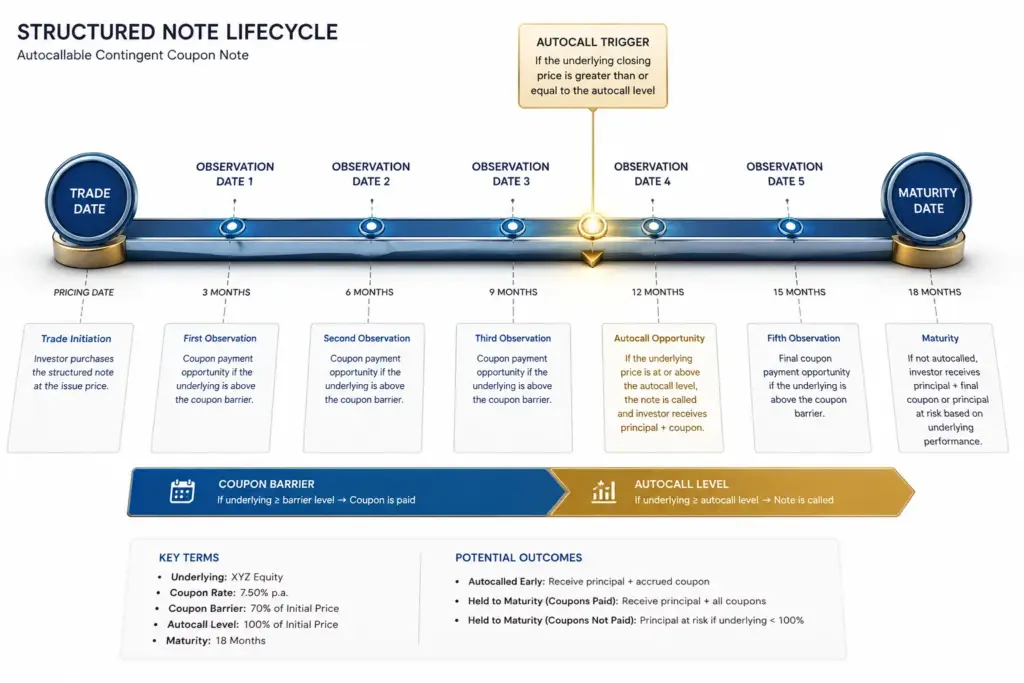

An autocallable product is a type of structured note — a pre-packaged investment that combines a debt instrument with one or more derivatives. What makes it “autocallable” is a built-in feature: under certain conditions, the product can redeem itself early, automatically, before its scheduled maturity date.

Unlike a traditional bond where you simply wait for maturity and receive your capital back with interest, an autocallable note monitors the performance of an underlying asset — typically a stock, index, or basket of equities — at specific points in time. If that asset meets a predefined price condition on any of those observation dates, the note is “called” — meaning it terminates early and the investor receives their principal plus a predetermined coupon.

This structure is part of the broader universe of structured products, which are engineered to deliver specific risk-return outcomes that standard market instruments cannot provide on their own. Understanding the basics of how these products are constructed gives you a much stronger foundation before diving into the autocall layer specifically.

What Does "Autocall" Actually Mean?

When someone says a product has been “autocalled,” what has actually happened?

When a product is autocalled, it means the note has been redeemed early — triggered automatically because the underlying asset’s price was at or above a specified level on an observation date. The investor does not need to take any action. The mechanism fires on its own, hence the name “autocall.”

Let’s say a structured note is linked to a major stock index, set with a 2-year maturity, and observed quarterly. If, on the first quarterly observation date, the index is trading at or above its initial level (the strike price set at inception), the autocall fires. The product ends, and the investor receives 100% of their capital back plus the agreed coupon — often a fixed annual rate paid pro-rata for the period held.

This early redemption is generally considered a positive outcome for investors, as they receive their return faster than expected. However, it also means the investment horizon is uncertain — the note might last three months or three years, depending entirely on market conditions.

This uncertainty in duration is one of the defining characteristics that distinguishes autocallable products from other types of structured products such as capital protection notes or simple participation structures, which have fixed maturities with no early exit mechanism.

How Do Observation Dates Work?

What are observation dates, and how frequently do they occur in a typical autocallable note?

Observation dates are scheduled points in time during the life of a note when the product’s underlying asset price is checked against the autocall trigger level. Think of them as “checkpoints” — if the asset passes the test on any checkpoint, the note redeems. If not, it moves on to the next checkpoint.

Most autocallable notes use quarterly or annual observation dates, though monthly structures also exist for more active yield-generation strategies. Here’s how a typical structure looks:

- Inception (Day 0): The initial price of the underlying asset is recorded. This becomes the “strike” or reference level.

- Observation Date 1 (e.g., 3 months in): If the asset is at or above the strike, the note is called. If not, it continues.

- Observation Date 2 (6 months in): Same test applied again.

- This continues until maturity if no autocall has been triggered.

The observation frequency directly impacts the probability of early redemption and the overall yield of the product. More frequent observation dates increase the chance of early redemption — but products with many observation windows typically offer slightly lower coupons to compensate for that higher probability.

For investors managing portfolio duration and cash flow planning, understanding observation date structures is essential — particularly when considering wealth management and structured notes as part of a broader asset allocation strategy.

What Is the Autocall Barrier?

What is the autocall barrier, and how does it affect whether the product gets called or not?

The autocall barrier — sometimes called the autocall trigger level — is the price threshold the underlying asset must reach or exceed on an observation date for the note to be redeemed early. It is typically expressed as a percentage of the initial (strike) price.

For example, if the autocall barrier is set at 100%, the underlying asset simply needs to be at or above its starting price on any observation date for the note to call. Some products set the barrier lower — say, 90% or 95% — to make early redemption more likely even in modestly declining markets. Others set it higher — say, 105% — to add a slight growth requirement before redemption occurs.

There is also a concept called a “step-down autocall,” where the trigger level decreases over time. For instance:

- Observation 1: Trigger at 100%

- Observation 2: Trigger at 97%

- Observation 3: Trigger at 94%

This step-down feature increases the probability of autocall in later periods and is commonly used in notes where issuers want to offer investors higher coupons while still managing redemption probability over time. It’s a design choice that directly reflects the trade-off between yield and the likelihood of holding the note to full maturity.

Understanding barrier structures is part of what makes structured products genuinely flexible instruments — each can be engineered to match a specific market outlook and investor preference.

Ready to Explore Structured Notes?

Access institutional-quality structured products through PhillipCapital DIFC.

How Are Coupons Structured in Autocallable Notes?

How does the investor actually earn income from an autocallable product?

The coupon in an autocallable note is the return paid to the investor upon early redemption — or in some structures, periodically throughout the note’s life. There are two main coupon models:

Fixed Coupon on Autocall

In the most straightforward structure, a fixed annual coupon rate is agreed at inception. If the note is called after one year, the investor receives 100% of principal plus one year’s coupon. If called after six months, they receive principal plus half the annual coupon rate. The rate is often higher than what comparable bonds or deposit products offer, which is the primary appeal.

Memory (Accumulating) Coupon

Some autocallable notes use a “memory coupon” feature. If the product does not meet the barrier on an observation date and no coupon is paid at that point, the coupon does not disappear — it is “remembered.” On the next observation date where the autocall does trigger, all previously missed coupons are paid out alongside the current one. This structure is designed to reward investors who hold through a period of underperformance, providing a catch-up payment when the market recovers.

Conditional Coupon (with a Separate Coupon Barrier)

More sophisticated structures include a separate, lower coupon barrier — distinct from the autocall trigger. For example, the autocall trigger might be at 100% of the initial price, but a coupon might still be paid as long as the underlying is above 70% of the initial price. This means investors can receive income even in periods of moderate market decline, adding a layer of yield resilience to the structure.

This layered design makes autocallable notes particularly attractive to investors seeking income above what is available in fixed income markets, while accepting defined and bounded risk exposure. Those familiar with bonds and debentures will recognise the income-oriented appeal, though autocallable notes typically carry more complexity and equity-linked risk.

What Happens If the Product Is Never Called?

What is the investor’s outcome if the underlying asset never reaches the autocall trigger throughout the note’s entire life?

If none of the observation dates result in an autocall, the note runs to its scheduled maturity date. At this point, the capital protection barrier — a separate and lower level than the autocall trigger — becomes the critical factor.

Here’s how it typically works at maturity:

- If the underlying asset is at or above the capital protection barrier (e.g., 60% or 70% of the initial price): The investor receives 100% of their principal back. No coupon may be paid, but capital is returned intact.

- If the underlying asset has fallen below the capital protection barrier: The investor’s return is directly linked to the performance of the underlying. For instance, if the underlying has fallen 50% and the barrier was set at 60%, the investor would receive back only 50% of their invested capital — a direct participation in the loss.

This is the key risk in autocallable products: the downside at maturity if markets have significantly underperformed. That’s why understanding the barrier level and the underlying asset’s historical volatility is critical before entering any autocallable position.

This scenario also illustrates why these products are not suitable for all investors — risk appetite, investment horizon flexibility, and an understanding of structured product behaviour are essential prerequisites. If you’re building knowledge from the ground up, starting with structured product basics gives context to where autocallables fit within the broader landscape.

Who Should Consider Autocallable Products?

What type of investor profile is typically well-suited for autocallable structured notes?

Autocallable products are generally best suited for investors who:

- Have a moderately bullish to neutral market outlook on the underlying asset or index.

- Are comfortable with uncertain investment duration — they could be repaid in three months or three years.

- Seek enhanced income compared to traditional fixed income, and are willing to accept equity-linked downside risk in exchange.

- Understand that early redemption is a feature, not a failure — being called is typically the intended positive outcome.

- Have sufficient portfolio diversification so that one structured note does not represent a concentration risk.

Autocallable notes are widely used by family offices, high-net-worth individuals, and institutional investors who want tailored risk-return profiles that the standard market cannot deliver off the shelf.

For investors in the UAE and DIFC who want access to such instruments through a regulated and established broker, institutional services at PhillipCapital DIFC are structured to support sophisticated clients seeking exactly this kind of exposure.

Speak to a Structured Products Specialist

Get guidance tailored to your investment profile and goals.

Key Takeaways

Autocall mechanics sit at the intersection of structured finance and investor behavioural insight — built to reward market stability and patience with above-market returns. Here’s what to carry forward:

- An autocall trigger is the price level the underlying must reach on an observation date for early redemption to occur.

- Observation dates are pre-scheduled checkpoints — quarterly, annual, or otherwise — where the trigger is tested.

- Step-down barriers make early redemption progressively easier over time, often paired with higher coupon rates.

- Coupon structures vary: fixed, memory (accumulating), or conditional — each suited to different investor preferences and risk tolerances.

- At maturity without a call, the capital protection barrier determines whether principal is preserved or exposed to loss.

- These products suit investors with flexible time horizons, income focus, and moderate risk appetite.

- Always assess the underlying asset, barrier levels, and issuer credit quality before committing capital.

Autocallable products are powerful tools — but like any financial instrument, their value depends on how well they match your investment objectives. Speak with a qualified advisor to understand how these structures may fit your portfolio.

Frequently Asked Questions (FAQs)

Can I lose money with an autocallable note?

Yes. If the underlying asset drops significantly and stays below the capital protection barrier at maturity, your principal is at risk. The loss mirrors the asset’s decline — not capped, not cushioned. This is the core trade-off: higher potential income in exchange for defined downside exposure in severe market conditions.

Is being autocalled early a good thing or a bad thing?

Generally, it’s a good thing. Early redemption means you receive your full principal back plus the agreed coupon — faster than expected. The only downside is reinvestment risk: you now need to find a new home for your capital, possibly in a lower-yielding environment.

What happens to my coupon if the product isn't called on an observation date?

It depends on the note’s structure. In a standard note, no coupon is paid that period and the product continues. In a memory coupon structure, the missed payment is carried forward and paid out in full on the next successful observation date. Always check which coupon type applies before investing.

What's the difference between the autocall barrier and the capital protection barrier?

They serve two completely different purposes. The autocall barrier determines whether the note redeems early — it’s checked on each observation date. The capital protection barrier (also called the knock-in level) only matters at maturity if the note was never called. Breaching the capital protection barrier at maturity is what puts your principal at risk. The two levels are usually set far apart — for example, an autocall trigger at 100% and a capital protection barrier at 60–70%.

Disclaimer:

Trading foreign exchange and/or contracts for difference on margin carries a high level of risk, and may not be suitable for all investors as you could sustain losses in excess of deposits. The products are intended for retail, professional and eligible counterparty clients. Before deciding to trade any products offered by PhillipCapital (DIFC) Private Limited you should carefully consider your objectives, financial situation, needs and level of experience. You should be aware of all the risks associated with trading on margin. The content of the Website must not be construed as personal advice. For retail, professional and eligible counterparty clients. Before deciding to trade any products offered by PhillipCapital (DIFC) Private Limited you should carefully consider your objectives, financial situation, needs and level of experience. You should be aware of all the risks associated with trading on margin.

Rolling Spot Contracts and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 78% of our retail client accounts lose money while trading with us. You should consider whether you understand how Rolling Spot Contracts and CFDs work, and whether you can afford to take the high risk of losing your money.

Barrier Levels and Payoff Impact

Barrier Levels and Payoff Impact Introduction Structured products often look...

Read More

Continuous vs Discrete Observation

Continuous vs Discrete Observation Table of Contents Introduction What Does...

Read More

Barrier Levels and Types

Barrier Levels and Types Introduction Structured products are built around...

Read More

Contingent Conversion Features

Contingent Conversion Features Introduction Structured products have evolved considerably over...

Read More

Early Redemption Features

Early Redemption Features Table of Contents Introduction What Is an...

Read More

Coupon Payments in Autocalls

Coupon Payments in Autocalls Table of Contents Introduction What Is...

Read More

Observation Dates

Observation Dates Introduction If you have ever explored structured products...

Read More

Autocall Mechanics

Autocall Mechanics Introduction If you’ve come across the term “autocallable...

Read More

Autocallable Structures

Autocallable Structure Table of Contents Introduction What Is an Autocallable...

Read More

Knock-In and Knock-Out Features

Knock-In and Knock-Out Features Table of Contents Introduction What Are...

Read More

Participation Structures in Structured Products

Participation Structures Maximizing Market Opportunities: A Guide to Participation Structures...

Read More

Zero Capital Protection

Zero Capital Protection Understanding Zero Capital Protection: Risks, Rewards, and...

Read More

Full Capital Protection

Full Capital Protection Understanding Full Capital Protection in Structured Products:...

Read More

Partial Capital Protection

Partial Capital Protection Partial Capital Protection: The Strategic Bridge Between...

Read More

Capital Protection Structures

Capital Protection Structures Strategic Wealth Preservation: A Comprehensive Guide to...

Read More

How Structured Products Work

How Structured Products Work A Complete Guide for Investors Table...

Read More

Components of Structured Products

Components of Structured Products A Detailed Guide for UAE Investors...

Read More

Introduction to Structured Products

Introduction to Structured Products In today’s dynamic financial landscape, traditional...

Read More